Post by Admin/YBB on Apr 14, 2021 6:30:02 GMT -6

ENERGY COMPLEX is a broad mixture of energy EQUITIES, energy FUTURES-based funds, energy distribution entities with tax-preferences [MLPs] and alternative/RENEWABLE energy. So, it has aspects of mainstream investing as well as alternatives. It is now among the smallest of 11 GICS sectors [S&P, MSCI]. Energy EQUITY ETFs can be subdivided into exploration and production [E&P – XOP, IEO, PXE], diversified energy producers [XLE (concentrated; also has options), IYE, FENY, VDE, RYE (equal-weight)], oil-servicing [OIH, IEZ, XES]; for specific COMPANY names, look at the top holdings of these ETFs. Crude oil FUTURES-based ETFs include USO [K-1], BNO [K-1], OILK [1099]. Partnership forms K-1 make tax filings bit complex and those are received after mid/late-March, so early tax filings are not possible. ETNs are really debt instruments with additional complications and are not discussed here. Master limited partnerships [MLPs] are pass-through entities that have tax-preferences on the distribution of qualified income. Most of the distributions are return of capital [ROCs] that are not taxed but reduce the cost-basis, so the taxes are deferred until sale. These have seen lot of restructuring as oil industry has gone through boom-and-bust cycles. Companies can be upstream {E&P – VNOM, SDLP, NRP], midstream [distribution via pipelines – WES, SMLP, SHLX, PAA, PSXP, WMB], downstream [refining, retail distribution – TGP, SUN, SPH]. The idea that midstream MLPs may not be sensitive to oil prices didn’t work in practice. Midstream MLP ETFs include AMLP, EMLP, MLPA, MLPX; these generate 1099s, not K-1s that are generated for MLPs held directly.

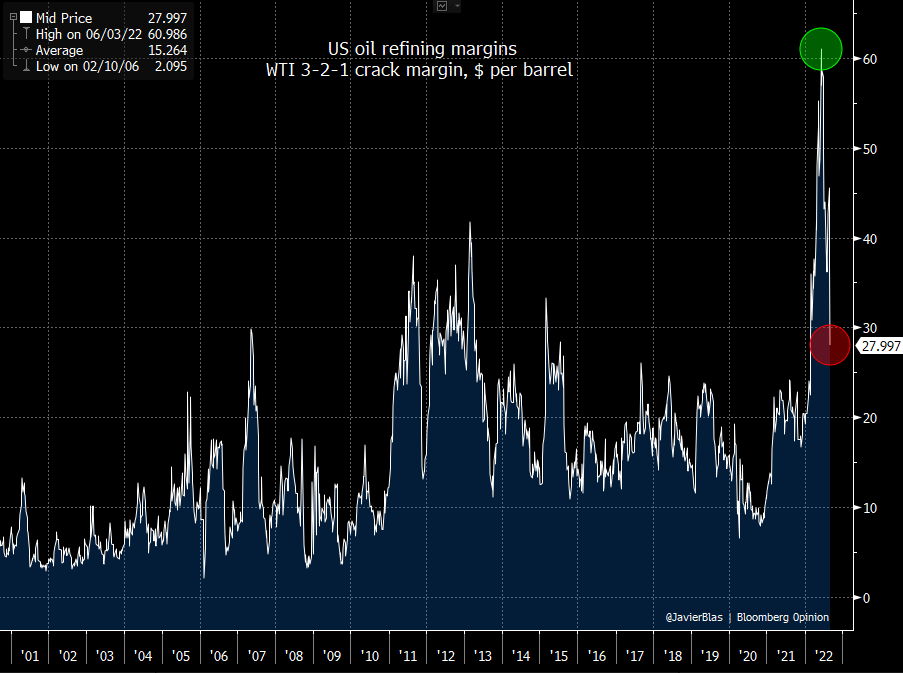

FACTORS affecting energy include geopolitical, OPEC/OPEC+, Middle East, severe weather, natural disasters, regulations, alternative or renewable energy, growing ESG trend, the US FRACKERS as swing producers. There are additional considerations such as NATURAL GAS is byproduct of oil production and much of it has to be used domestically or flared/wasted; it can be exported only as liquified natural gas [LNG] and that requires complex handling at the source, for transportation and at terminal points. Considering extraordinary differentials in the prices of natural gas in the US and overseas, these extra costs for LNG are justified. REFINING of crude oil produces a huge variety of products and that mix can be adjusted only to some extent. For example, refineries produce GASOLINE, DIESEL, jet-fuel, heating-oil, etc irrespective of the local demand; the excess distillates are exported. Gasoline is transported unblended [RBOB – reformulated blendstock for oxygenated blending] to reduce its corrosive effects on transmission infrastructure, and final blending [and branding] is done only at local terminals before distribution to retail pumps by tanker-trucks.

REGULATIONS require mixing of some ETHANOL with gasoline; common E10 has 10% ethanol; only special car models can use E85 with 85% ethanol. So, the energy markets also affect the agricultural markets [sugarcane, corn, beets, potatoes] as large sugar producers can make sugar or industrial ethanol depending on the crops and the demand for sugar and gasoline. Use of biofuels [methane, syngas, ethanol, methanol, butanol, biodiesel, ether additives, etc] is also increasing. ALTERNATIVE energy sources are nuclear, wind, solar, hydro. RENEWABLE sources [wind, solar] generate energy intermittently, so energy STORAGE technology becomes critical. Growing ESG considerations are driving the move towards clean/green energy. There are projections that alternate or renewable energy will dominate one day, and electric-vehicles [EVs] may replace gasoline/diesel-consuming internal combustion engines [ICE]; but gas-electric hybrids may be around for a long while. However, the reality is that fossil-fuels based energy will remain dominant for the next 30-50 years. Large energy companies will have to adjust with changing technologies and industrial/consumer demands.

FACTORS affecting energy include geopolitical, OPEC/OPEC+, Middle East, severe weather, natural disasters, regulations, alternative or renewable energy, growing ESG trend, the US FRACKERS as swing producers. There are additional considerations such as NATURAL GAS is byproduct of oil production and much of it has to be used domestically or flared/wasted; it can be exported only as liquified natural gas [LNG] and that requires complex handling at the source, for transportation and at terminal points. Considering extraordinary differentials in the prices of natural gas in the US and overseas, these extra costs for LNG are justified. REFINING of crude oil produces a huge variety of products and that mix can be adjusted only to some extent. For example, refineries produce GASOLINE, DIESEL, jet-fuel, heating-oil, etc irrespective of the local demand; the excess distillates are exported. Gasoline is transported unblended [RBOB – reformulated blendstock for oxygenated blending] to reduce its corrosive effects on transmission infrastructure, and final blending [and branding] is done only at local terminals before distribution to retail pumps by tanker-trucks.

REGULATIONS require mixing of some ETHANOL with gasoline; common E10 has 10% ethanol; only special car models can use E85 with 85% ethanol. So, the energy markets also affect the agricultural markets [sugarcane, corn, beets, potatoes] as large sugar producers can make sugar or industrial ethanol depending on the crops and the demand for sugar and gasoline. Use of biofuels [methane, syngas, ethanol, methanol, butanol, biodiesel, ether additives, etc] is also increasing. ALTERNATIVE energy sources are nuclear, wind, solar, hydro. RENEWABLE sources [wind, solar] generate energy intermittently, so energy STORAGE technology becomes critical. Growing ESG considerations are driving the move towards clean/green energy. There are projections that alternate or renewable energy will dominate one day, and electric-vehicles [EVs] may replace gasoline/diesel-consuming internal combustion engines [ICE]; but gas-electric hybrids may be around for a long while. However, the reality is that fossil-fuels based energy will remain dominant for the next 30-50 years. Large energy companies will have to adjust with changing technologies and industrial/consumer demands.