|

|

Post by Admin/YBB on Dec 24, 2022 19:38:13 GMT -6

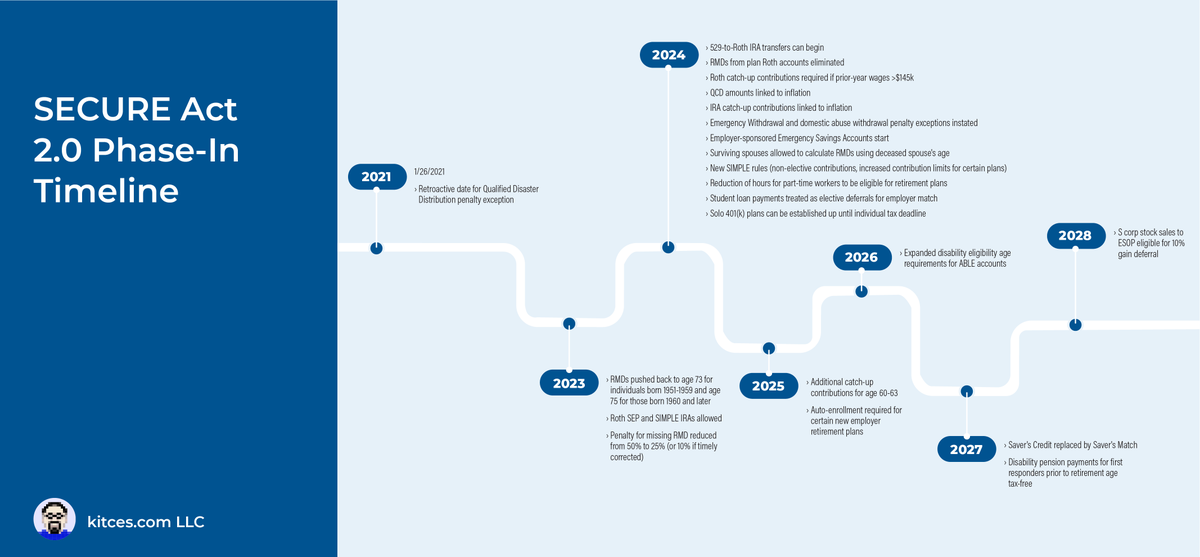

Secure Act 2.0 was passed along with the huge budget bill. It includes important changes for retirement savings and planning (401k/403b/457b, Roth IRA/Roth 401k/Roth 403b, RMDs, QLACs, QCDs, etc), educational 529/Roth IRA, disability 529-ABLE, LTCI premiums, etc. More details will be added later. www.cnbc.com/2022/12/23/secure-2point0-clears-congress-will-bring-changes-to-retirement-system.html401kspecialistmag.com/passed-secure-2-0-awaits-bidens-signature-after-1-7t-spending-bill-clears-house-friday/www.aaii.com/investor-update/article/29463-changes-to-retirement-savings-included-in-the-omnibus-billbipartisanpolicy.org/blog/what-made-it-in-secure-2/assets.kpmg/content/dam/kpmg/us/pdf/2022/12/tnf-secure-act-section-by-section-dec20-2022.pdfwww.finance.senate.gov/imo/media/doc/Secure%202.0_Section%20by%20Section%20Summary%2012-19-22%20FINAL.pdfwww.klgates.com/SECURE-20-Act-Legislation-Includes-Significant-Changes-to-Individual-Retirement-Accounts-1-31-2023www.kitces.com/blog/secure-act-2-omnibus-2022-hr-2954-rmd-75-529-roth-rollover-increase-qcd-student-loan-match/Kitces has posted a chart showing the timeline when various provisions of Secure 2.0 kick in, LINK.  |

|

|

|

Post by Admin/YBB on Dec 25, 2022 7:27:10 GMT -6

|

|

|

|

Post by Admin/YBB on Sept 4, 2023 10:03:39 GMT -6

A more details discussion of aggregation of RMDs from partially annuitized accounts included in Secure 2.0. ritaus.org/secure-2-0-offers-a-powerful-retirement-income-planning-opportunity/"..... SECTION 204 OF SECURE 2.0 Under the RMD rules, individuals must begin receiving a minimum amount from their retirement plans and IRAs each year upon reaching age 73 (to be later increased to 75), based on their remaining life expectancy. Section 204 of SECURE 2.0 directs Treasury to amend its RMD regulations to eliminate a “penalty on partial annuitization” under qualified defined contribution plans and IRAs. The new rule is immediately effective, without the need for new RMD regulations to implement it. The issue addressed by section 204 can be explained as follows. Under the pre-SECURE 2.0 RMD rules, annuitizing a portion of one’s retirement savings generally produces a higher benefit payment for the individual than the RMD amount the individual would have been required to withdraw if they had not annuitized. This occurs naturally because annuity payments are generally higher than the required withdrawals under similar economic assumptions using the method the RMD rules apply to non-annuitized accounts.1 The problem is that when computing the RMD amount that an individual must withdraw from her non-annuitized account, she does not get any credit under the RMD rules for the fact that the annuity payments from the annuitized portion are higher than the minimum withdrawals would have been.2 As illustrated below, SECURE 2.0 provides individuals with the option of taking credit for that higher payment. Let’s assume that Ruth turns 75 years old in 2023 and her retirement savings consist entirely of a $475,000 traditional (non-Roth) IRA. In December Ruth decides to purchase a single life annuity using a little less than half ($200,000) of her traditional IRA to supplement her Social Security benefits. That annuity will pay Ruth $18,500 per year as long as she lives, starting in January 2024.3 The new RMD rule for partial annuitizations in SECURE 2.0 comes into play beginning with Ruth’s RMD calculation for 2024: Old RMD Rule. Under the old rule for partial annuitizations, which Ruth may still choose to use, Ruth’s RMD for 2024 would equal the sum of (1) her $18,500 annuity payment that year, plus (2) a calculation based on the account balance of the nonannuitized portion of her IRA as of December 31, 2023. That balance was $275,000, so Ruth’s RMD for her nonannuitized account in 2024 would be $275,000 divided by 23.7 (her life expectancy factor from the IRS’s uniform lifetime table), or $11,603. Thus, in 2024 Ruth would receive her $18,500 annuity payment, and she must withdraw a minimum of $11,603 from the non-annuitized portion of her IRA. New RMD Rule. If Ruth instead elects to use the new rule in SECURE 2.0, her 2024 RMD is calculated differently. We explain this calculation in more detail below, but, in short, Ruth would first add the values of the annuitized and non-annuitized portions of her IRA as of December 31, 2023. On that date, the non-annuitized account was valued at $275,000, and the annuity had a present value of $200,000,4 for a total value of $475,000. Next, a total RMD amount is calculated as her total value of $475,000 divided by 23.7 (the same uniform lifetime table factor used above), or $20,042. Finally, Ruth’s annual annuity payment of $18,500 is subtracted from $20,042, leaving a remainder of $1,542. Based on this calculation, in 2024 Ruth would be required to withdraw only $1,542 from her nonannuitized IRA, in addition to receiving her $18,500 annuity payment....." |

|

|

|

Post by Admin/YBB on Feb 10, 2024 15:23:23 GMT -6

|

|